Written by Cláudio Afonso | [email protected] | LinkedIn | Twitter

Following the earnings results reported on Thursday, Citi analyst Jeff Chung release a new note reiterating the firm’s $87 price target on NIO shares, an upside potential of 362.3% from the previous closing price. The firm had raised NIO‘s price target back in November 2021 from $70 to $87.

The analyst enhanced that the EV maker is about to ramp up the production now that its F1 (factory number one) is back to pre-Covid levels plus the opening of NEO Park (F2) in the third quarter of the year.

In addition, Chung added that NIO‘s order inflow reached a new all-time high in May and the company’s expansion to another four markets later this year after entering Norway in 2021: Germany, the Netherlands, Sweden, and Denmark.

BE THE FIRST ONE TO GET THE NEWS

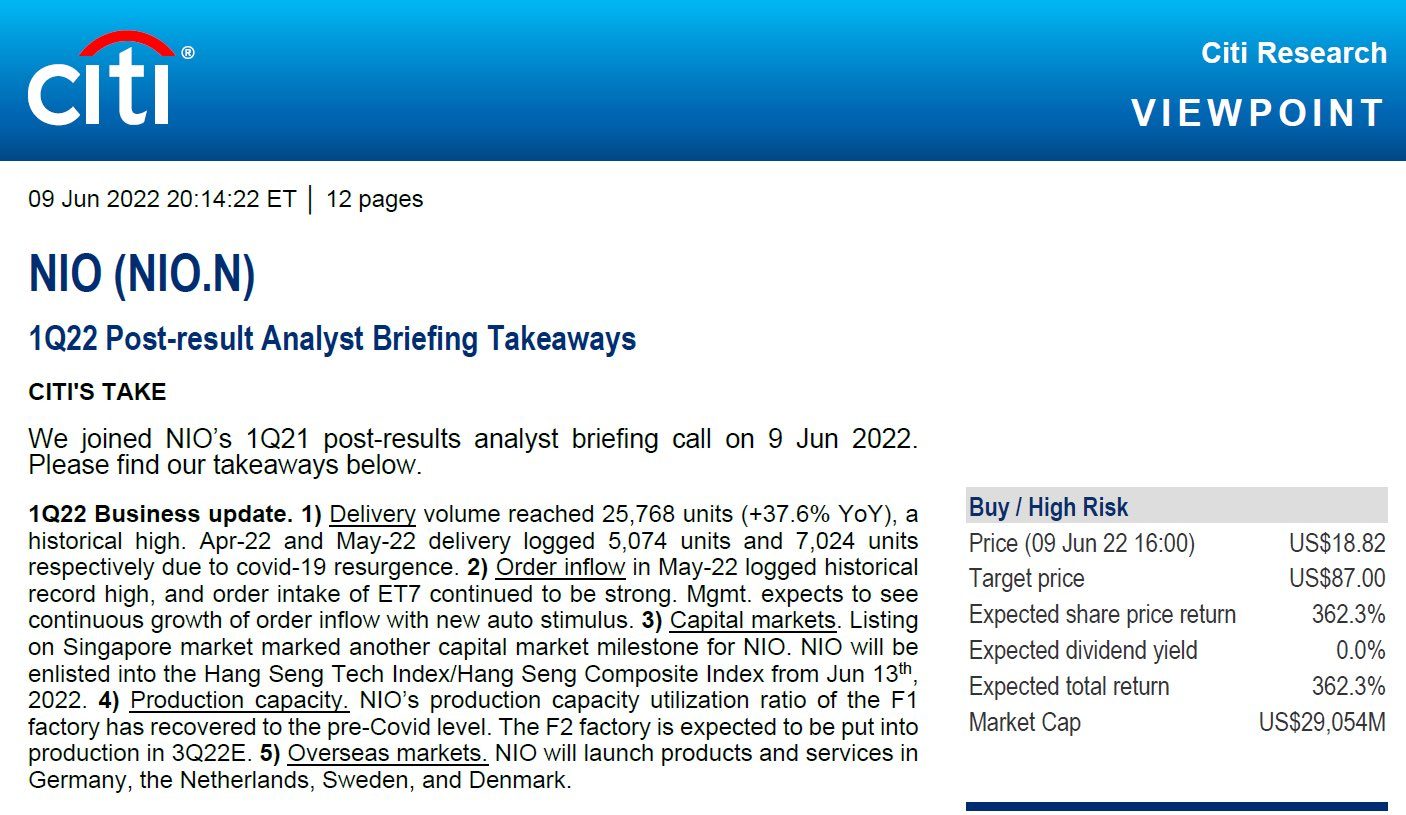

Citi’s Take

1) Delivery volume reached 25,768 units (+37.6% YoY), a historical high. Apr-22 and May-22 delivery logged 5,074 units and 7,024 units respectively due to covid-19 resurgence.

2) Order inflow in May-22 logged historical record high, and order intake of ET7 continued to be strong. Mgmt. expects to see continuous growth of order inflow with new auto stimulus.

3) Capital markets. Listing on Singapore market marked another capital market milestone for NIO. NIO will been listed into the Hang Seng Tech Index/Hang Seng Composite Index from June 13th, 2022.

4) Production capacity. NIO’s production capacity utilization ratio of the F1 factory has recovered to the pre-Covid level. The F2 factory is expected to be put into production in 3Q22E.

5) Overseas markets. NIO will launch products and services in Germany, the Netherlands, Sweden, and Denmark.

Earlier this week, the analyst had already commented the results saying NIO to deliver more than 40,000 vehicles in the third quarter which would represent a new record for the company and an average monthly pace of 13,333 units delivered.

For the second quarter of 2022, NIO said that expects to deliver between 23,000 and 25,000 vehicles, representing an increase of approximately 5.0% to 14.2% from the same quarter of 2021.

“Overall 1Q GPM was below consensus due to sales mix changes and asymmetric battery cost & car-price hikes; However at the bottom line level the net loss was narrowed QoQ due to effective cost saving on SG&A,” Chung said.

“NIO gave very strong June sales guidance ceiling at 13k units, or 84% MoM, which may potentially implies 3Q volume may exceed 40k level (in our view), with ample re-rating upside risk ahead on margins and asset-turns,” the analyst added.

BE THE FIRST ONE TO GET THE NEWS

During NIO’s conference call (Full Transcript here), Jeff Chung asked William Li about the margin outlook for the second quarter and also about NIO’s pace for the upcoming months:

“So I have two questions. One is the second quarter GP margin outlook. So it looked like the high-margin products as a percentage of sales in the second quarter could reach about 37% versus 17% in the first quarter. I think this is one of the positives that may potentially lift up the GP margin trend.

And secondly is that there has been some MSRP hike recently. And we would like to know how much of the sales volume from the second quarter has been a price hike versus the first quarter. Obviously, this is the first question.

And the second question is that our new model cycle suggests that our current aging products, three products, is going to turn into six new products into the next 6 to 12 months. So my question is whether the third quarter production capacity can reach above 48,000 units since, by referring to Tesla, we saw a strong week-on-week and month-on-month recovery from the past weeks. And my understanding is that a lot of our supply, auto part suppliers are overlapped with the Tesla. So, if Tesla recover fast would that mean that we are going to enjoy the similar pace into June and the third quarter?”, the analyst asked.

William Li, NIO CEO

“Thank you for your question, Jeff. Starting from April, we actually updated our agreement with our battery supplier CATL. And right now, our battery cost is connected with the raw material indexes. So basically, it means that if in the second quarter we can see the battery cost is going to significantly increase compared with that of the first quarter, and this is going to affect of vehicle gross margin performance, but there’s going to be some latencies.

The battery prices increase in the prior month is going to be reflected in the battery cost of the later months and this is going to incorporate it into offer bigger gross margin performance. According to the current forecast and the market trend, we can see the battery cost is going down a little bit starting from May and we have also taken some measures, for example, increasing our product prices. This is going to help us improve our performance in the third quarter.

Right now, we are still delivering vehicles without the price adjustment and we expect to start to deliver the vehicles with the price adjustment starting from the third quarter because our business model is made to order or order to delivery.

So just now you have also mentioned that our products with higher gross margin is also going to kick in, in terms of the performance of the vehicle gross margin. Just as the ET7 that is launched in the second quarter and we expect the production of ET7 is going to gradually ramp up starting from June. And then starting from the third quarter is going to maintain at a normal level.

Overall speaking, we believe our vehicle gross margin is going to face a higher pressure in the second quarter. So this is mainly due to the battery cost impact. The vehicle gross margin of the second quarter is going to be lower compared with that of the first quarter. But with the price adjustment, we expect we are going to start to deliver the vehicles with higher prices starting from the third quarter which is going to contribute to our vehicle gross margin.

With the production capacity expansion in the F1, we expect that this is going to start to improve the overall production output starting from June. Of course, it will need some time to gradually ramp up the production, but we believe the vehicle production is not going to be a bottleneck. And the demand is not an issue for us. The main challenges that we’re facing right now is the supply chain, especially in terms of the chipset and also the production capacity of our suppliers. We are very confident of our delivery performance starting from the third quarter” William Li concluded.

Earlier this week, NIO surpassed the U.S.-based Lucid Motors in Market cap becoming the third biggest EV maker after Tesla and BYD. On Monday, NIO stock opened higher at $18.99 and immediately saw buy pressure gapping up to a new 6-weeks high of $19.80 resulting in a Market Cap value of $31.482 billion. In parallel, Lucid stock went down to $18.80 per share which, considering the 1.67 billion shares outstanding, results in a market cap value of $31.412 billion.

NIO will hold a conference to officially launch the new SUV model NIO ES7 on June 15, at 20:00 in Shanghai timezone. The company will start receiving reservations on the evening of the conference and the orders will start to be locked in July with the first deliveries expected as soon as the end of August.

Written by Cláudio Afonso | [email protected] | LinkedIn | Twitter