Written by Cláudio Afonso | [email protected] | LinkedIn | Twitter

HSBC analyst Yuqian Ding raised on Tuesday the firm’s price target on LI Auto shares to $47.00 while maintaining a Buy rating. Ding expects “the continuous volume ramp-up of L9” from the third quarter onwards and “more new model offerings including NEV (New Energy Vehicles) type in 2023-24e “. Based on the last closing price of $39.13, the new price target represents a 20.11% upside potential on the shares.

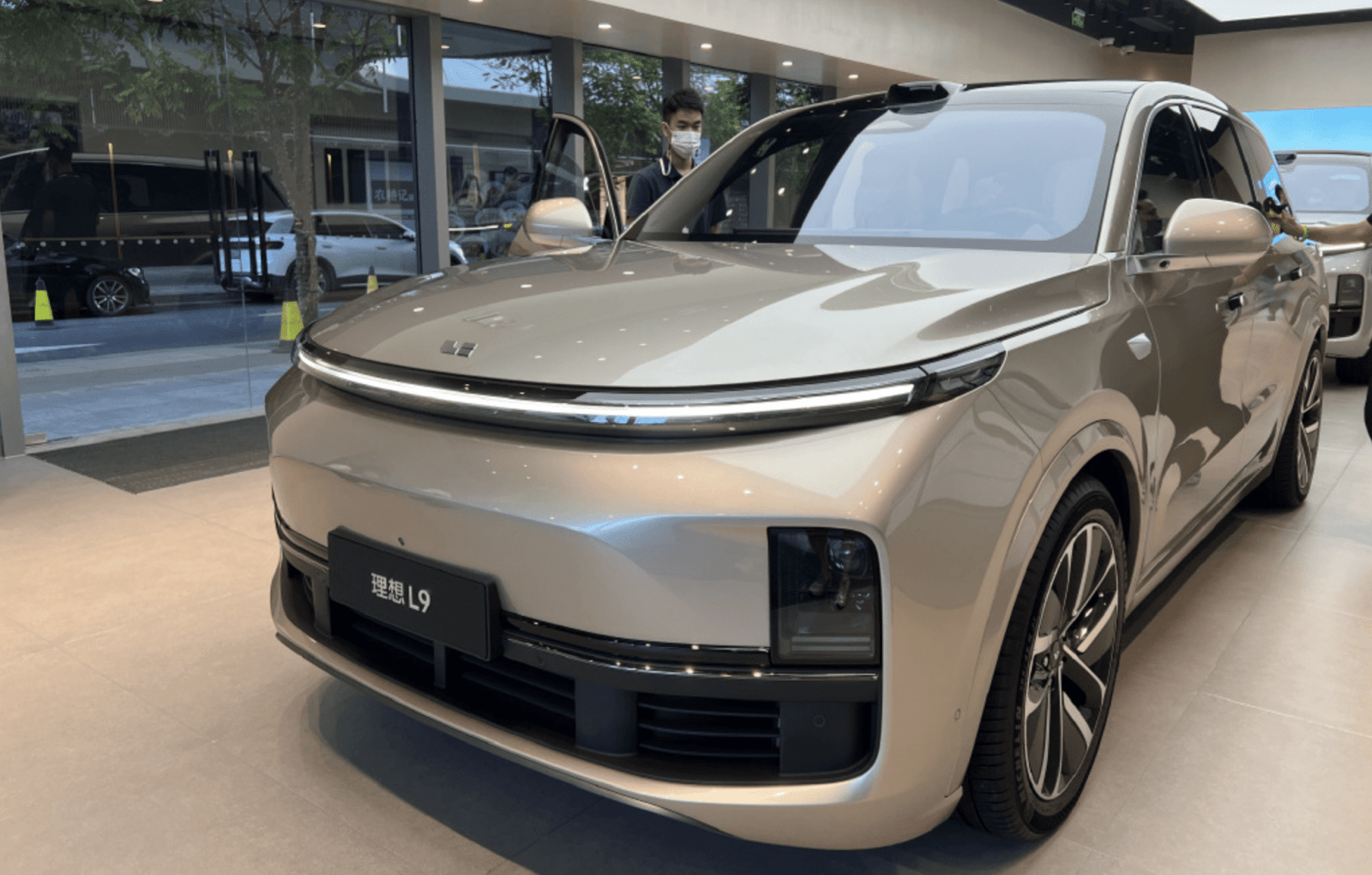

The analyst said, “Accelerating product cycle to boost volume and earnings growth: On 21 June, Li launched its second full-sized EREV SUV model L9, priced at RMB459.8k, which is targeted for family users offering more space as well as higher intelligence level”.

“According to the company, the delivery of L9 will begin in August 2022, and we expect the continuous volume ramp-up of L9 from 3Q22 onwards and more new model offerings including NEV type in 2023-24e would further boost the company’s volume and earnings growth. Our volume growth estimates are 84% for 2023e from 72% previously and 94% for 2024e from 44%,” Ding added.

Initially scheduled to launch on April 16, the second model of LI Auto was released on June 21 and needed only 72 hours to reach over 30,000 orders, as the company announced on Friday. Last Sunday, via its official app, LI unveiled that will commence the test drives for its SUV model on July 16.

The L9 model features a self-developed high-efficiency range-extending electric system with a 44.5kWh battery pack achieving 1315km battery life (CLTC operating conditions), of which the battery life is 215km.

The SUV features “an intelligent driving computing power platform that includes two Nvidia Orin-x processors, the total power reaches 508Tops, and the dual processors are redundant with each other’s computing power, making the intelligent driving system more stable,” the company added.

Written by Cláudio Afonso | [email protected] | LinkedIn | Twitter